Tuesday, February 28, 2012

Proceed With Caution

This link from Media Matters shows just how cold-hearted certain members of the media can be. Read at your own risk, it may cause high blood pressure.

Are Poor People Just Getting What They Deserve????

Saturday, February 25, 2012

Ten years later...

Ten years later...

...the first flower of spring bloomed.

Ten years later...

...we still fly the flag in his memory.

Ten years later...

... his youngest son who was only seven back then, lit the fire today. I notice he needs a shave. He is seventeen.

Ten years later...

... we stand together as a family and remember. The bad memories are burning away. We keep the good memories. Always.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

It really helped to write my posts of the past few days. I hope our story will reach the ears of those who can help change things. Please share it, if it moves you to do so. But now that I have put it into words, I can put it out of my thoughts. That in itself gives me peace of mind.

Onward...

Friday, February 24, 2012

All of our money was gone. :(

Our personal savings were depleted.

All the college money I had been saving for the kids was wiped out. I had to cash in the savings bonds I had saved for all three of them, in order to pay bills the insurance wouldn't cover. I had to pay these bills, or the doctors would refuse to see us, plus we wouldn't be able to order needed medical supplies.

Andy's former coworkers brought us a carload of groceries and paper goods. We were overwhelmed with their generosity, but my oldest son felt ashamed. We had never needed to accept charity before. I told him that it was their blessing to give to us, and we needed to not be so prideful as to spoil their blessing. It did feel weird to be in that position, though.

It was obvious that we were sinking fast. Even with the kindness of those coworkers and our church, family, and friends, it wasn't going to be enough; soon we would have to decide between making our house payment and utilities, or paying for the medical expenses. I decided to heed my friends' advice and take my case to the State Insurance Commission to see if they could light a fire under the tail of the insurance company. In order to do that, I had to take a day off from work....!! (Expletive deleted!)

I was afraid that the people at the Insurance Commission would be as cold and rude as some of the people at the insurance company and the collection agencies, so I took my best friend with me for moral support. However, the lady at the agency was very sweet and sympathetic. The only problem was, she could do nothing to help me.

"If you had a traditional health plan or an HMO I could help you," she said.

I asked, "Aren't an HMO and an EPO the same thing?"

"They are very similar, but EPO means the insurance is employee owned, so they set their own rules, for the most part."

She jotted down a few notes for me, explaining that there was a small chance that I might be able to get some help because of something called the ERISA act, but I would have to take it up with the Federal Department of Labor, and it would require an enormous amount of documentation.

She sighed and said, "I wish I could guarantee that this will work. I know this is a lot for you to do with so much on your plate already."

It was a good thing that my friend was driving; I never would have made it home through all my tears and as hard as I was shaking.

Long story short, I did begin the process with the Department of Labor, but soon after that Andy's condition deteriorated and he was hospitalized for several months. About the same time, my new insurance plan through the school plus his Medicare Disability kicked in. Over the next few months my former insurance company began to pick up the overdue bills, but there were some that were missed. I never did get reimbursed for any out-of-pocket expenses that I had paid, because that also would have taken considerable paperwork, and by then Andy was so critical the only thing I could think about was the probability I was going to lose him. Oh, that and the fact that I was still taking care of my kids, working full time, and trying to maintain our home.

If you missed my earlier posts, the reason I took on a different job in the middle of all this is Andy was too sick to watch the kids anymore while I was at work, so I needed a different position so I could work during the same hours they were in school. The new job had great hours, but quite a pay cut came with it. Under the new health care rules of 2012, he would be insured as soon as I started my new employment because insurance companies no longer can turn a client down for pre-existing conditions. If it were that way ten years ago, I never would have had to mess around with Cobra.

The hours and hours I spent on all the insurance red tape cheated us both out of much of our last time together...

... and that was undoubtedly the most expensive toll of all.

"Please remit payment immediately."

I have to smile, while sorting through the box with all these papers, I found this:

I must have been planning on using coupons to offset the $26,000 bill in the next photo. Despite my best efforts, Andy's medical bills were piling up unpaid.

As time went on, collection efforts became more serious. For instance, the State of Oklahoma gave us the choice of paying a bill in full, or signing over part of our tax return.

They did generously include a form for Andy to sign, but I put it aside when Andy had to be rushed to ICU and then I forgot about it.

I was still receiving a huge amount of denials, despite paying almost half of my monthly salary to cover the Cobra insurance. I was advised to talk to the State Insurance Commission. Surely they could help me! Right???

My other full time job

It wasn't enough that I was taking care of a house and my kids, spending time with my critically sick spouse, and working at the school 5 days a week. I had another full-time job taking care of insurance paperwork!

The insurance company instructed me to send certified letters to every doctor, lab, radiology company, pharmacy, equipment company, ambulance, etc. with copies of the updated insurance cards that finally arrived in my mailbox. As you can see, it took a bit of time, energy and money, but I did it.

The denial letters slowed down a bit after I sent out the updated information, but they never stopped completely, even after Andy died. I continued to contact the insurance company, and tried to pay the bills or make arrangements, but some slipped through the cracks. One of the years after he died, I was garnished for an ambulance bill at Christmas time. Nice, huh?

Thursday, February 23, 2012

"Who's On First" at the Insurance Company?

The bottom of this post has the 4 pages of the timeline mentioned in yesterday's entry. For the sake of brevity, I am posting the highlight of the timeline seperately.

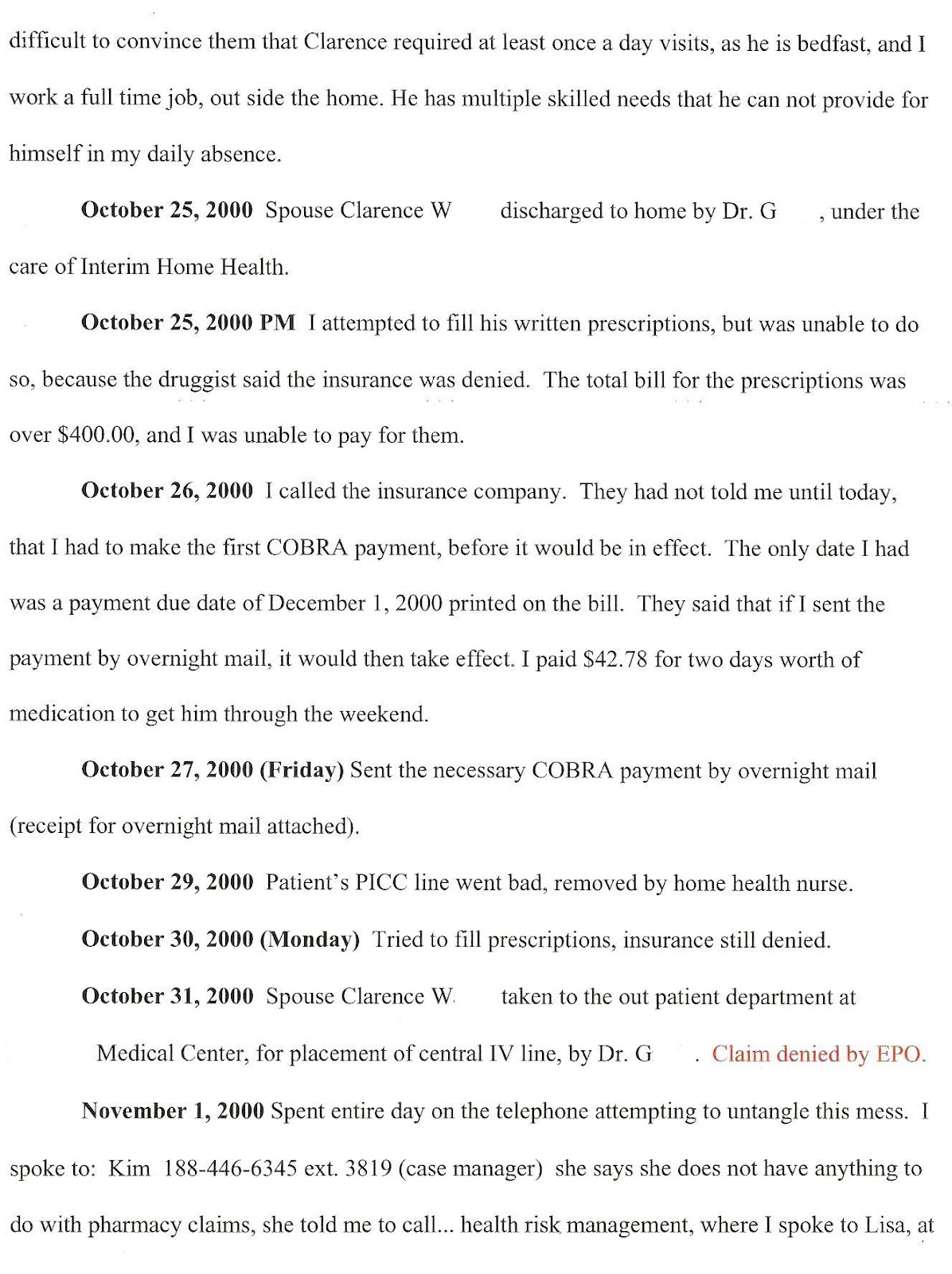

Setting the scene: Andy was discharged from the hospital 5 days earlier. I had been attempting to get his antibiotics filled at the local pharmacy, but the insurance was denying payment. The medications were over $400.00, and after all the out-of-pocket expenses I had already covered, I didn't have the money to purchase the medicine. This story actually is hysterical in a macabre sort of way. At the time, however, I wasn't laughing, I was sobbing and pulling my hair out!!! Read on...

~~~~~~~~~~~~~~~

Spent entire day on telephone attempting to untangle this mess. I spoke to Kim 188-446-ext 3819 (case manager). She says she does not have anything to do with pharmacy claims, she told me to call Health Risk Management, where I spoke to Lisa at 1-800-255-5541.

She told me to call Express Scripts at 1-800-234-4879, where I was told to call the Cobra Connection at 1-800-733-9110, where they told me to call the eligibility department at 1-800-357-9597, where they told me I needed to call Express Scripts (again) where I spoke to Samantha, who told me she didn’t know how to help me, but transferred me to ext. 59105 where I spoke to Rosie at the Michigan Call Center.

Rosie finally was able to find record of my payment to Cobra, and told me the reason why the prescriptions were being denied was because the ID# was now supposed to be my husband’s Social Security # rather than mine. I had not been informed of this before. (In fact, the letter I had received from Cobra had said that I should continue to use my previous ID cards!)

I returned to pharmacy, instructed the pharmacist to use my spouse’s SS#. Insurance was still denied. I ended up obtaining the prescriptions without the help of the EPO."

~~~~~~~~~~~~~~~

I didn’t mention in my letter to Nancy exactly how I obtained the medicine because I wanted to protect the pharmacist… he had been working with me on this since Andy had been released from the hospital 6 days earlier. He took pity on me because by this time I was bawling my eyes out and Andy desperately needed the antibiotics… so that dear pharmacist gave me the antibiotics at my former co-pay rate and said, “This is ridiculous. They can straighten this out after your husband gets started on his medicine.”

If you want more comedy, here is the rest of this particular saga. Or skip it, that's okay, it's pretty much just more from the same circus. Have I mentioned how much I hate insurance companies???

Click on each page to enlarge.

Wednesday, February 22, 2012

A Sample of Insanity

How in the world can I put this out there so it makes some kind of sense to others? It doesn't even make sense to me! After all these years it still is very difficult to figure out the order and organization of that pile of paperwork. The dates blend together, there are mountains of different forms, and mountains of requests for further info. It would be an impossible task to show the magnitude of the issue without showing each individual form, and I won't do that to you! How boring would that be??? :)

I guess this letter would be a good beginning. I wrote this to my director of Human Resources during the early days of Andy's terminal illness. Can you imagine? This was just the beginning! Sorry, I can't bring myself to re-type all of this, so I did a photo scan of each section... click to enlarge...

I had left my full-time position at the hospital to work for the school, because Andy had become too sick to work and to care for John and Shelby while I worked. His insurance was canceled after his medical retirement, but he had to wait 6 months to qualify for Medicare. I took the Cobra insurance through the hospital because of his pre-existing condition, and it would take several months before my new insurance through the school would cover him.

Yes, they really asked if I had family members or neighbors to take care of his medical needs!!

What Nancy and Cindy advised me to do was make up a timeline of events so they could look into why all the bills were continuing to be denied. My head was already spinning, and now I had to try to piece together everything! My best friend came over that evening to help me put together all the paperwork and try to construct a timeline. It took us over 8 hours, working together.

Tomorrow I will post that timeline. Until then, thanks for listening.

Monday, February 20, 2012

Preparing for an Awesome Bonfire

This will be a catharsis of sorts.

The ten year anniversary of Andy's death is rapidly approaching. Over these years I have written many items regarding grief, recalled many happy and bittersweet memories, and poured out my emotions in general. One thing I haven't told is the awful story of the mountains of medical bills we dealt with, and how the walls kept closing in as I wrestled with the insurance company to make sure Andy received the benefits that my insurance was expected to cover; the medicines and treatments that were keeping him alive.

In addition to the anguish and fear we both felt as Andy slowly headed toward the light, I was also dealing with this:

These photos show the reason for my red-hot hatred of the insurance industry. It would not have upset me if these were statements of bills paid. No, that's not how it worked then, and that's not how it works today. These are piles and piles of denial letters and subsequent correspondence. These represent the bald-faced fact of health insurance companies...

They are not here to help us stay healthy or regain our health.

They are here to make a profit. Period.

At the time, I told my family and friends, "I am seeing the future of medical care and insurance, and it isn't pretty, folks."

We were a couple of the earliest baby-boomers to see what's in store for us if drastic changes aren't made. President Obama's new health care plan is a baby step in the right direction, but it doesn't go far enough. To prevent this from happening in YOUR future, we need a single payer system. For a system to make any family with a critically ill loved one have to go through this paperwork nightmare, to keep the patient receiving their treatments, is unconscionable.

During the next few days I will be posting a few of the insurance "highlights" that we went through. As recently as two years ago I wouldn't have been able to consider doing this. Even still, thumbing through this stuff makes the panic rise in my chest, and like invisible hands are wrapped around my throat, slowly suffocating me.

Maybe my story will help someone else.

I know it will help me to tell it.

At the end, I am going to mark the tenth anniversary of Andy's death with a lovely bonfire. I wish it were that easy to burn up all the bad memories.

But it's a start.

Thursday, February 16, 2012

My career meme- School Nurse

I know there are so many of these going around that people are getting sick of them, but I just had to join in the fun! Hope you all enjoy. :)

(Click on photo to enlarge)

P.S. I made it all by myself, I didn't copy it. Aren't you proud of me?

Subscribe to:

Posts (Atom)